Posted 9 августа 2023, 07:38

Published 9 августа 2023, 07:38

Modified 9 августа 2023, 15:55

Updated 9 августа 2023, 15:55

New mortgage rates: is it worth taking out housing loans at all?

Real estate expert Irina Safina: we expect an increase in apartment prices

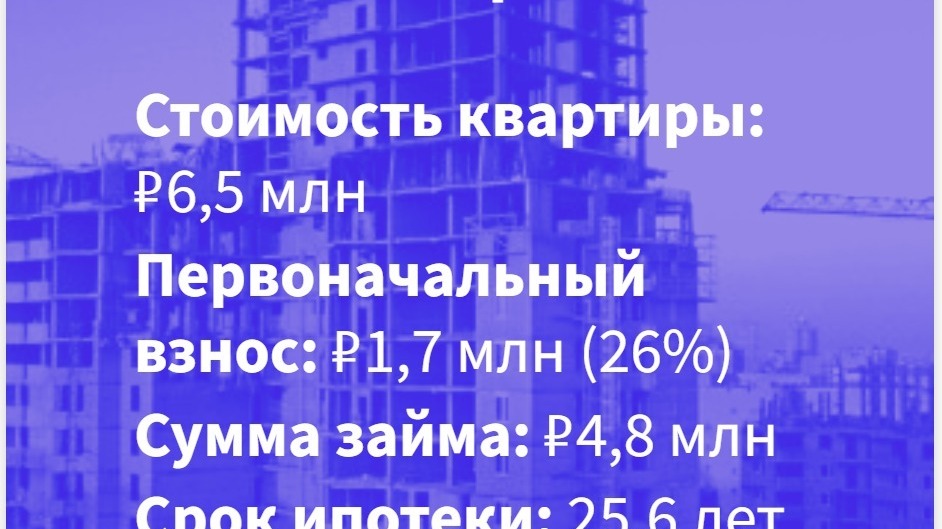

Own apartment in Russia is a luxury that only wealthy people can afford for cash. For the rest there is a mortgage. According to the Central Bank, the average mortgage size in May 2023 amounted to 4.8 million rubles, and the repayment period stretched for 25.6 years. Analysts «HOUSE.The Russian Federation» calculated that the initial payment on average is 26% of the value of the property.

It turns out such an average mortgage: a person buys an apartment for 6.5 million rubles, pays 1.7 million immediately, and stretches the remaining amount for 307 months. If this is a new building, then according to the new rates of Sberbank, the monthly payment will be 48.25 thousand rubles, and the overpayment will be 10.018 million rubles. Borrowed 4.8 million from the bank — paid interest in the amount of more than 10 million rubles. If you take an apartment in the secondary, then the monthly payment will be 49.3 thousand rubles, and the overpayment will be 10.34 million. That's how an almost imperceptible difference in percentages affects regular payments and the final overpayment.

Mortgage or rental housing?

You pay like for several apartments, but you get only one. Taking into account the fact that the average cost of renting a «two-bedroom apartment» in Russia is estimated by «CYAN.Analysts» is 30680 rubles, for the price of a new apartment, taking into account all overpayments, you can rent an apartment for almost 45 years. But who knows how prices will change in 5, 10 or 20 years? With rental housing, you are completely dependent on the market, and mortgage payments will remain that way.

After seeing such calculations, it is very easy to refuse to buy your own home in favor of a rented one. Moreover, there are many options — now even the state has profitable houses. According to Maria Rumyantseva, Head of the SAMPLE agency and the Internet forum PRONedvizhimost, monthly payments for a rental apartment can be significantly lower than mortgage contributions.

— To assess the benefits of «Rent vs Purchase with a mortgage», it is necessary to compare monthly payments. For example, in Moscow now you can still rent a one-room apartment for 30-35 thousand rubles a month. And when we calculate monthly mortgage payments for the buyer of the same one-bedroom apartment with a minimum initial payment, then, depending on the complex, we get a payment of about 60 thousand rubles for 30 years.

There are a lot of fears when buying an apartment with a mortgage: suddenly the apartments will become cheaper, suddenly the house will be demolished under the integrated territorial development program (CRT) without the consent of the tenants, suddenly due to a decrease in income, the opportunity to repay the mortgage will disappear. With rental housing, everything is easier. Not your own — it's not a pity. There was a need — I moved to a new place. In addition, as the partner of the real estate agency Capital Estate Irina Safina notes, the increase in mortgage rates will not lead to an increase in prices for rental housing.

— Mortgage and the rise in the cost of rental real estate are not connected in any way. Rental real estate primarily depends on demand, on the number of people who have come to the city. Since last year there was a large outflow of people in Moscow who have not yet returned, it is not necessary to talk about an increase in rental prices.

But Vasily Timofeev, general director of the St. Petersburg construction company Community Solutions, is sure that people should not have such a choice at all.

— This comparison does not make sense, since it solves fundamentally different tasks. When deciding on a mortgage, we are talking about the acquisition of property, long-term life planning, finding your home, where you will live for many years, where you will arrange everything to your liking, maybe leave it to your children. Buying a home is a security, because regardless of your financial condition, this housing will remain with you. Rental housing has the advantage of flexibility. You can change the area, move closer to work, increase housing with the growth of the family, in the case of shift or temporary work in another city, there is no need to invest significant money. A serious drawback is the impossibility of long—term planning. The standard rental contract is 11 months, so it is impractical to make repairs for yourself, and you will not be able to live in a rented apartment as in an apartment made for yourself.

Take a new building or a secondary one?

Which is better: to take a new building at the announced 11,4% or a secondary one at 11,7%? In fact, everything is much more complicated, since the market is distorted by preferential government mortgage programs. Now all Russians have access to a «Mortgage with state support at 8-9% (sometimes even less when applying for insurance and electronic registration of the transaction). The main thing is that a new apartment should be bought from a developer or under a DDU contract, the initial payment was at least 15%, and the loan amount did not exceed 12 million rubles in Moscow, St. Petersburg, Moscow and Leningrad regions and 6 million rubles in all other regions. There are also specialized preferential programs for residents of the Far East, IT specialists and families with children. Vladimir Putin said today that since the beginning of the year, about 400 thousand families have used preferential mortgages, and according to the CIAN, 78% of mortgage loans for new buildings are now issued with the involvement of state subsidies.

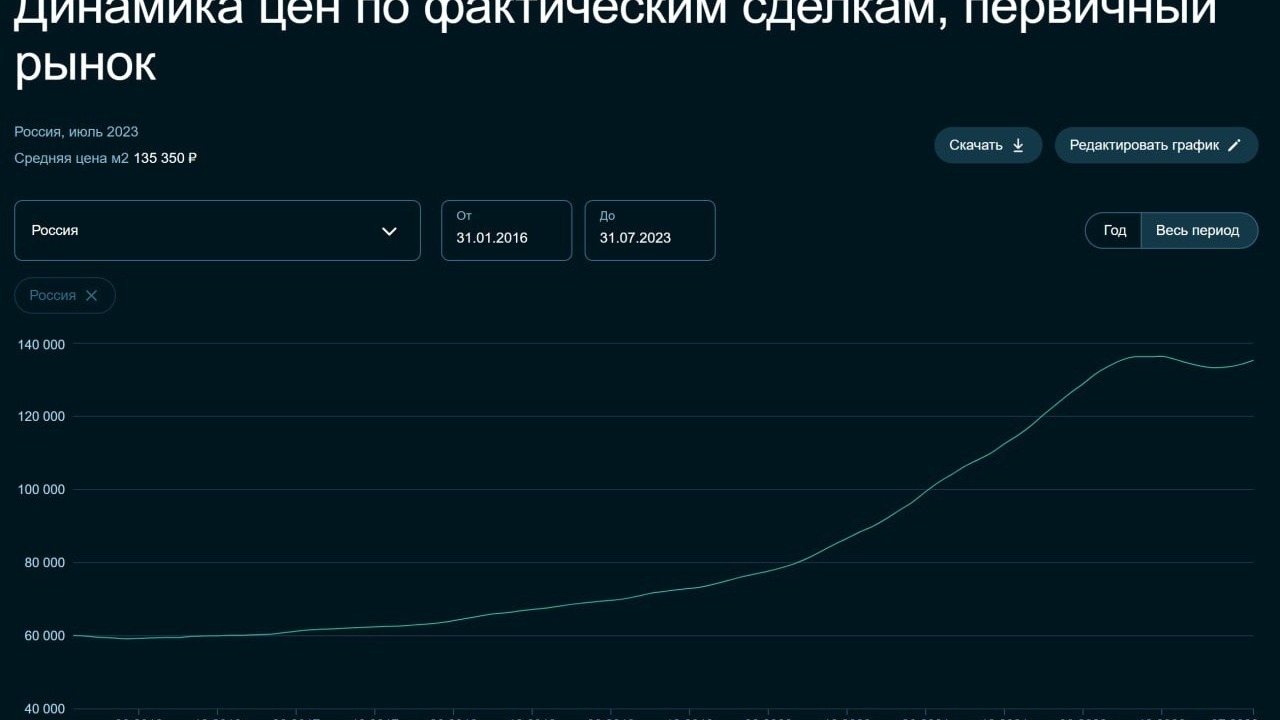

According to the Central Bank, thanks to state programs, the weighted average mortgage rate on housing under construction in June 2023 was 6,12%. It looks very good against the background of Sber's 11,7% on the secondary. But there is one caveat: the price difference between new buildings and secondary buildings reached 40% by the end of the first quarter!

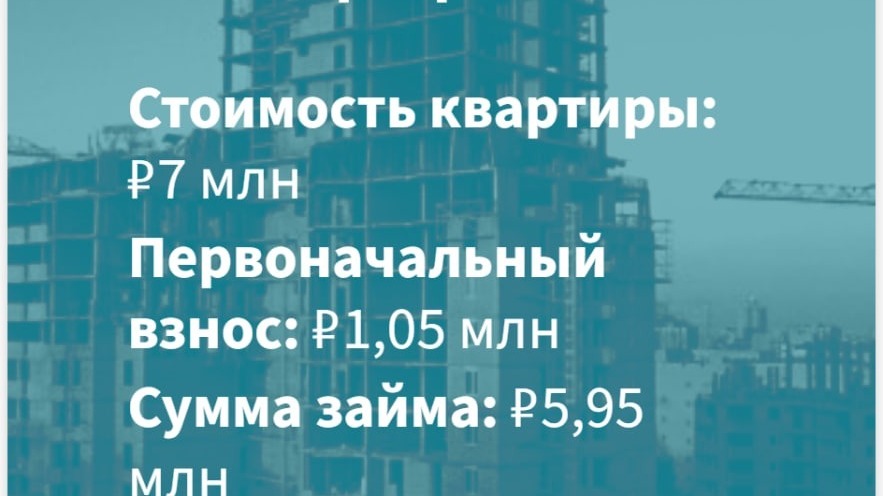

If you take a new building for a conditional 7 million rubles, then the initial payment will be 1.05 rubles. We stretch the remaining 5.95 rubles for 307 months. Monthly payments will amount to 38.4 thousand rubles, and the total overpayment — 5.84 million.

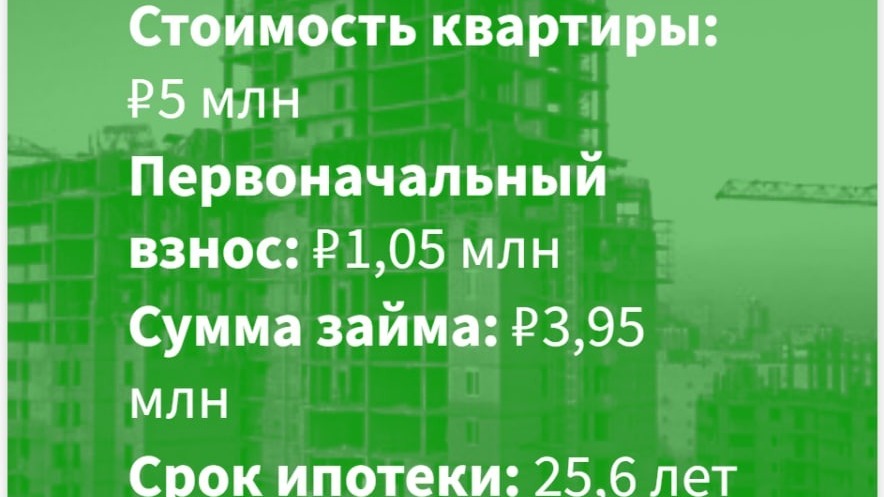

If you take a similar apartment on the secondary market, then according to statistics, it should cost 5 million rubles. Having the same 1.05 million on hand, you will have to borrow 3.95 million. Monthly payments will amount to 40.6 thousand rubles, and the total overpayment — 12.46 million.

It turns out that cheaper does not mean more profitable. Each specific case must be carefully calculated depending on the interest rates offered.

Should I buy an apartment right now or wait

The apartment was chosen, but is it worth buying it now or wait — suddenly the market will sink and real estate will become cheaper, suddenly the rates will become lower? History shows that cheaper apartments in Russia is a myth. In foreign currency, they may sink, but in rubles — almost never. According to Sberindex, for the entire history of observations since 1996, new buildings have become cheaper only once — last year. And even then the drawdown was short and not strong.

Irina Safina also holds the opinion that it will only be more expensive from now on.

— Apartments definitely will not become cheaper. On the contrary, we expect prices to rise, especially in the premium and luxury real estate segment, because there is a shortage of supply with good finishes. And mortgage rates will not decrease either — the Central Bank raises the key rate and there are no grounds for a reduction.

Does not doubt such a prospect andMaria Rumyantseva.

— Apartments will not get cheaper. This is an axiom of the real estate market. Seasonal and situational price fluctuations at the level of 5-10% are possible, the terms «market collapse» or «price drop» are used only by journalists to create a picture of the apocalypse. Real estate has been and remains a reliable means of saving money and generating additional income.

The Central Bank's desire to gradually abandon preferential state programs also warms up the market. It all started 3 years ago with a rate of 6,5%, and now banks can give 8-9% per annum on state support. Also, Elvira Nabiullina systematically liquidates mortgage programs with minimum rates or minimum down payment from banks and developers.

And do not expect that real estate will instantly become cheaper without state programs. Irina Safina notes that the preferential mortgage was not the main reason for the rise in price of apartments.

— Preferential programs did not have much effect on the price growth. Developers calculate the financial model of the project even before it enters the market. That is, prices would rise in any case.

Apartments are expensive now, but they will be even more expensive. Dreams of high-quality and affordable housing for millions of Russians will remain dreams.